Structuring the payment leg of an international property purchase is one of the most critical—and most misunderstood—parts of a cross-border real estate transaction. A clear structure reduces delays, protects both parties, and ensures legal compliance. Unlike domestic purchases, where both buyer and seller operate within the same banking and legal framework, international deals introduce variables such as currency conversion, cross-border banking regulations, and time zone differences. Without a well-defined payment structure, even the most promising deal can unravel at the last minute.

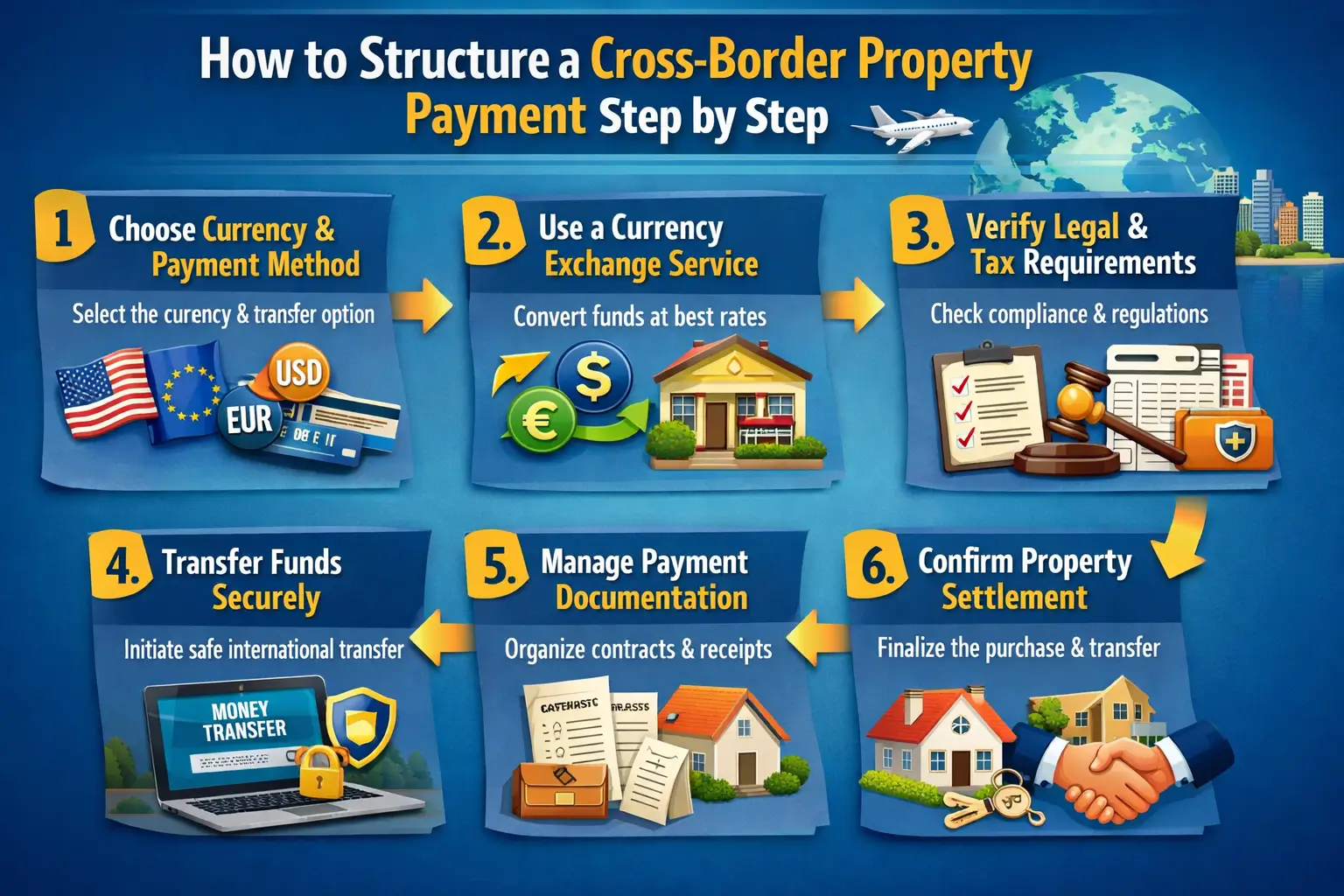

Step 1: Define the Transaction Milestones

Most property purchases involve multiple stages, including reservation deposit, private purchase contract, and final deed signing. Each milestone should be mapped to a specific payment condition and legal requirement. The reservation deposit, typically 5-10% of the purchase price, secures the property and takes it off the market. The private purchase contract (often called the "promissory contract" in civil law jurisdictions) may require an additional payment. The final deed signing involves the balance of the purchase price. Understanding these milestones and their financial implications is essential for structuring payment timelines that align with legal obligations.

Step 2: Align Currency Conversion With Legal Deadlines

Currency exchange should be scheduled with sufficient buffer to avoid settlement delays. Buyers should confirm cut-off times, intermediary bank processing, and compliance checks well before notary appointments. Currency markets operate on their own schedules, and a transfer initiated on a Friday may not settle until Tuesday or Wednesday, depending on the currency pair and banking holidays in both originating and receiving countries. Additionally, currency conversion rates can fluctuate significantly, so buyers should consider using forward contracts or limit orders to lock in favorable rates and protect against volatility.

Step 3: Use Escrow or Conditional Release Mechanisms

Escrow or conditional payment solutions ensure that funds are only released once contractual and legal conditions are satisfied. This protects both buyer and seller and prevents last-minute disputes at signing. In many Southern European countries, notaries play a key role in validating the transaction and ensuring that all conditions are met before funds are transferred. However, traditional escrow arrangements can be slow and opaque. Modern escrow platforms designed for cross-border real estate provide real-time visibility and automated release conditions, reducing the risk of delays and disputes.

Step 4: Coordinate With Notaries and Registries

Notaries and land registries operate on strict schedules and documentation requirements. Payment confirmation must be synchronized with these processes to avoid rescheduling or legal complications. A notary may refuse to proceed with the signing if funds are not confirmed in the seller's account or held in escrow with verifiable proof. This means that payment timing is not just a financial issue but a legal one. Buyers should work closely with their notary to understand exactly what proof of payment is required and by when, and ensure that their payment provider can deliver that proof in the required format and timeframe.

Step 5: Manage Documentation and Compliance Proactively

Cross-border payments trigger anti-money laundering and know-your-customer checks that can cause unexpected delays. Buyers should prepare documentation early, including proof of funds, source of wealth declarations, and identification documents. Having these ready before initiating the transfer can prevent compliance-related holdups. It is also advisable to work with payment providers that specialize in real estate transactions, as they understand the specific documentation requirements and can guide buyers through the process efficiently.

Step 6: Build in Contingency Time

Even with careful planning, unforeseen issues can arise. Bank holidays, technical glitches, or additional compliance requests can all delay settlement. Building in contingency time—typically two to three extra business days—between the scheduled payment date and the notary appointment provides a safety net. This buffer reduces stress and allows for last-minute adjustments without jeopardizing the closing date.

Conclusion

By structuring payments around legal milestones rather than treating them as simple bank transfers, international buyers can significantly reduce the risk of delays and failed transactions. A structured approach not only protects the buyer's investment but also builds trust with sellers, agents, and notaries, making the entire transaction smoother and more reliable. In a competitive market where timing is everything, having a clear and robust payment structure is a strategic advantage.